Table of Contents

- The Excel Framework We’ll Build (Watch Deal Lab Part 6 First)

- Why Arbitrage Needs a “Base Layer”: Resource Adequacy (RA), ELCC & NQC

- Building the Arbitrage Engine in Excel: From Spreads to Cash Flow

- Step 1 — Start with a simple arbitrage switch (the flag)

- Step 2 — Pull the price forecasts (charge and discharge) as time series

- Step 3 — Convert real prices to nominal (indexation)

- Step 4 — Compute energy per cycle (charge energy vs discharge energy)

- Step 5 — Profit per cycle → profit per year

- Step 6 — Keep the RA constraint visible

- Common Pitfalls and the Lender Lens (Keep It Underwriteable)

- Wrap-Up and Next Steps (Deal Lab + RVA Certification)

- FAQs

BESS Merchant Energy Arbitrage sounds simple on paper: charge when prices are low, discharge when prices are high, and pocket the spread. But if you’ve ever tried to translate that story into a lender-clean Excel model, you know the truth: Energy Arbitrage is rarely “buy low, sell high” in the real world. The economics are driven by a tight set of constraints—cycles, losses, deliverability, and price shapes—and if you don’t model those mechanics explicitly, your BESS Merchant Energy Arbitrage profits will almost always look better than what the asset can actually earn.

The problem isn’t that arbitrage doesn’t work. The problem is that most models skip the steps that turn a price spread into bankable cash flows. A realistic arbitrage engine has to answer four questions with precision:

How many cycles can the battery actually run?

Equivalent Full Cycles (EFCs) are the control knob for throughput. A battery might be physically capable of cycling daily, but in many real structures—especially when the project also sells contracted capacity—dispatch flexibility is limited. Your arbitrage upside is then “headroom monetization,” not unlimited daily spread capture.What price curve are you arbitraging—pure merchant or constrained?

In real deals, you often cannot charge at the daily minimum and discharge at the peak. The price curves you’re allowed to monetize may be constrained by contractual obligations, grid rules, or operational priorities. If you ignore that, you are implicitly assuming a “perfect trader” battery—something lenders won’t finance.How much energy do you buy vs. how much do you sell?

Losses are not a footnote. Round-trip efficiency, one-way conversion losses, and transformer/MV losses determine the gap between energy required to charge and energy you can deliver back to the grid. A correct model forces you to compute both paths explicitly—and it keeps your accounting discipline clean across AC/DC boundaries.Do availability and curtailment reduce merchant opportunity?

If the battery is unavailable, you can’t arbitrage. If it’s curtailed, you might not be able to inject energy when spreads are attractive. Whether you embed those effects in the EFC assumption or model them as explicit adjustment switches, the key is consistency—no double-counting, no missing haircuts.

That’s exactly what we’ll build in this article: a practical BESS Merchant Energy Arbitrage revenue engine in Excel that starts with charge/discharge price forecasts, applies cycles and operational constraints, converts energy correctly through the efficiency stack, and outputs clean profit metrics—per cycle and per year—that you can actually use in project finance modeling.

The Excel Framework We’ll Build (Watch Deal Lab Part 6 First)

Before we go into the mechanics, it helps to be crystal clear on what “good” looks like in BESS Merchant Energy Arbitrage modeling. The goal isn’t to create a complicated spreadsheet—it’s to build a transparent, auditable engine that turns a spread story into numbers you can defend in an investment memo or a lender model review.

At a high level, the framework has four building blocks:

Merchant price inputs (charge & discharge)

You need two time series: the average price you pay to charge and the average price you earn when discharging. In the Deal Lab model, these come from the Inputs Time Dependent sheet as annual forecasts (the kind of forecasts you’d typically receive from an independent market consultant). This is important: we’re not pretending we can simulate hourly dispatch inside a yearly project finance model. Instead, we create a clean container for forecast assumptions and build a disciplined translation to annual cash flows.

Throughput control via cycles (EFCs)

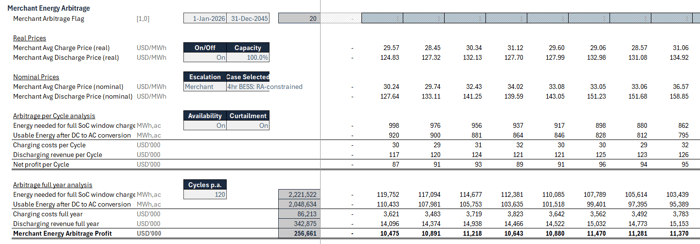

Cycles per year are the throttle. If you assume too many cycles, your BESS Merchant Energy Arbitrage profit will look amazing—but it will be economically and operationally unrealistic. If you assume too few, you’ll understate upside. In our RA + Arbitrage case (Case 5), the cycles are intentionally constrained (120 EFC/year) because the battery is primarily committed to a capacity product, leaving limited headroom for spread capture.Energy per cycle (charge vs discharge) with losses applied correctly

This is where most models quietly break. You don’t “buy 1 MWh and sell 1 MWh.” You buy more than you sell, because losses sit in the conversion chain. In the model we explicitly compute:

Energy required for a full charge (AC energy drawn from the grid, after switches for availability/curtailment if applicable)

Usable energy delivered back (AC energy injected to the grid, after efficiency and loss adjustments)

That AC/DC boundary discipline matters because revenues settle at the point of interconnection on an AC basis, while physics and degradation live on the DC side. If your math blurs that line, your BESS Merchant Energy Arbitrage cash flows won’t be lender-clean.

Cash flow outputs (per cycle and per year)

Once we have prices and energy, the economics become simple and intuitive:

Charging cost per cycle = charge price × charge energy

Discharge revenue per cycle = discharge price × discharge energy

Net profit per cycle = revenue − cost

Then scale it: multiply by cycles/year to get annual costs, annual revenues, and annual gross profit.

To make this as practical as possible, we recommend watching the Deal Lab lesson first—then coming back to this article as your “mental model + written reference” while implementing it in Excel.

🎥 Deal Lab Part 6 — BESS Merchant Energy Arbitrage Model in Excel

In that video, you’ll see the full BESS Merchant Energy Arbitrage block built step-by-step: pulling charge/discharge price forecasts with XLOOKUP, converting real prices to nominal using an index selection, computing charge and discharge energy per cycle with the correct operational adjustments, and translating it all into annual profit that actually drives the dashboard revenue mix. Once you’ve watched it, the next section of this article will walk you through the key assumptions behind the RA-constrained arbitrage setup—so your BESS Merchant Energy Arbitrage doesn’t accidentally assume a “perfect merchant” battery that the contract structure simply doesn’t allow.

Why Arbitrage Needs a “Base Layer”: Resource Adequacy (RA), ELCC & NQC

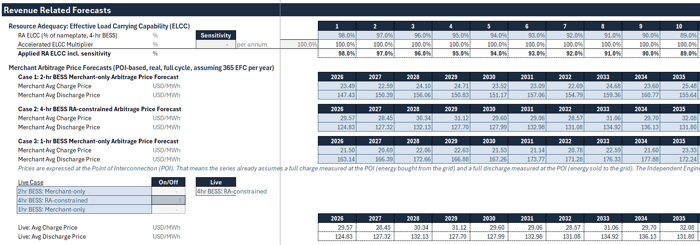

If you want your merchant upside to feel realistic in a project finance model, you need to start from the constraint, not from the spread. In Project Pulse Case 5, the battery isn’t a free-floating merchant trader—it’s a 4-hour resource adequacy asset first, with merchant arbitrage layered on top. That’s exactly why the Deal Lab uses a deliberately modest arbitrage throughput assumption (120 equivalent full cycles per year): the project has RA obligations, and arbitrage is only monetized with the headroom that remains.

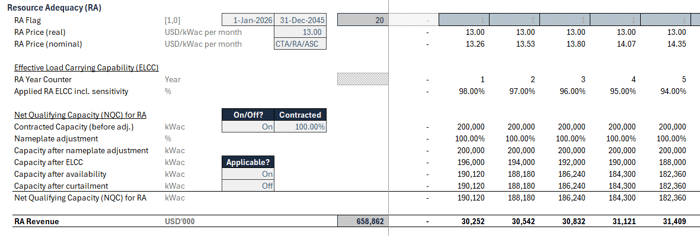

This context matters for BESS Merchant Energy Arbitrage because it changes both the economics and the credibility of the assumptions. In many markets, the RA payment is tied to the part of the battery that is accredited as reliable capacity. That accredited slice is not equal to 100% of nameplate forever. Instead, it’s governed by ELCC (Effective Load Carrying Capability), which is typically modeled as a time-dependent percentage that trends down as the grid becomes more saturated with storage.

The key idea in one sentence

A tolling contract pays for the battery’s contracted capacity directly, but an RA contract pays for net qualifying capacity (NQC)—the portion of nameplate that counts as reliable, which is nameplate × ELCC (and then adjusted for availability and other contract specifics).

In the model, this “base layer” is implemented cleanly and transparently:

You reuse most of the tolling agreement structure (flag, term, price, indexation, capacity basis).

Then you add what’s RA-specific:

a RA year counter (so you can map year 1–20 to an ELCC path),

an XLOOKUP-based ELCC time series (often provided by a market consultant),

and the NQC calculation that determines what actually earns the RA payment.

Why do we care in a merchant-focused article? Because once you understand the RA base layer, you understand why the arbitrage overlay is constrained, why the “perfect spread capture” assumption is wrong, and why a realistic BESS Merchant Energy Arbitrage model must reflect product priorities (RA first, merchant second). The RA revenue stabilizes the project and makes the structure more financeable, while arbitrage becomes the upside option that can improve equity returns without being fully underwritten for debt sizing.

🎥 Deal Lab Part 5 — BESS Resource Adequacy (RA) Revenue Model in Excel

In Part 5, you’ll see the RA block built on the operations sheet: starting from contract terms and a fixed $/kW-month capacity payment, then layering in ELCC to convert nameplate AC capacity into NQC, and finally translating that into annual contracted cash flows. Once that base layer is in place, the merchant overlay in Part 6 becomes far more defensible—because your BESS Merchant Energy Arbitrage is no longer an unconstrained “spread trade,” but a controlled monetization add-on sitting on top of a contracted capacity framework.

Building the Arbitrage Engine in Excel: From Spreads to Cash Flow

Now that the RA “base layer” is clear, we can focus on what actually makes (or breaks) merchant upside: translating charge/discharge spreads into bankable annual cash flows without accidentally overstating throughput or double-counting adjustments.

Here’s the clean sequence you want in Excel (and the same logic you follow in the Deal Lab model):

Step 1 — Start with a simple arbitrage switch (the flag)

The arbitrage flag is your on/off master switch. It keeps the model modular: you can run Case 5 with and without arbitrage and instantly see how much value is coming from merchant overlay versus contracted capacity. This is also what keeps the model audit-friendly—no hidden “merchant effects” lingering in formulas when the revenue stream is off.

Step 2 — Pull the price forecasts (charge and discharge) as time series

Arbitrage is driven by two annual price paths:

Average charge price (what you pay to buy energy from the grid)

Average discharge price (what you earn when selling back)

In a yearly model, you’re not trying to optimize hourly dispatch. You’re using forecast containers—typically provided by a market consultant—and consistently mapping them into cash flows. The important modeling discipline is traceability: your operations sheet should make it obvious which dropdown price case is selected and which rows in your time-dependent forecast table feed the revenue engine.

Step 3 — Convert real prices to nominal (indexation)

If your price forecast is “real” (today’s dollars), you still need to express cash flows in the model’s nominal currency framework. This is where index selection matters: the model multiplies real prices by the chosen escalation index, so your revenue and cost series stay consistent with inflation assumptions used across the rest of the project finance model.

Step 4 — Compute energy per cycle (charge energy vs discharge energy)

This is the core of “lender-clean” arbitrage modeling:

Energy needed to charge (AC from grid)

This is how many MWh you must buy to fully charge the usable state-of-charge window, after applying any availability/curtailment switches if you choose to reflect them explicitly.Energy delivered on discharge (AC to grid)

This is how many MWh you can sell back after the efficiency chain and conversion losses—typically lower than charge energy because round-trip losses are real economics.

If you keep your boundary discipline straight (what lives on AC vs DC), your outputs will “feel right” instantly: charge energy is slightly higher than discharge energy, and the difference is your efficiency loss expressed in MWh.

Step 5 — Profit per cycle → profit per year

Once prices and energy are correct, the economics become simple:

Charge cost per cycle = charge price × charge energy

Discharge revenue per cycle = discharge price × discharge energy

Net profit per cycle = revenue − cost

Then scale it:Annual charge cost = charge cost/cycle × cycles/year

Annual discharge revenue = revenue/cycle × cycles/year

Annual arbitrage profit = annual revenue − annual cost

This is where your “spread story” becomes a decision-grade number. You can see exactly what drives merchant upside: spreads, losses, and throughput—nothing else.

Step 6 — Keep the RA constraint visible

Because this is Case 5 in our BESS Deal Lab (RA + Arbitrage), your cycles assumption is intentionally not “as many as possible.” The logic is: RA product first, arbitrage second. That’s the difference between a merchant model that looks great and a merchant model that looks credible.

Common Pitfalls and the Lender Lens (Keep It Underwriteable)

The fastest way to overstate BESS Merchant Energy Arbitrage is to treat a constrained battery like a free merchant trader. In practice, the “spread” is only one ingredient—and most modeling errors happen when assumptions quietly contradict the physical or commercial boundaries of the asset.

Here are the pitfalls that matter most:

Too many cycles, not enough constraint. If the battery is committed to RA, you don’t get unlimited dispatch flexibility. Your cycles per year should reflect what’s actually left for arbitrage after contractual priorities are met. A conservative EFC assumption is often more credible than a “perfect daily cycle” assumption.

Perfect price capture. Real-world arbitrage is not “charge at the daily minimum, discharge at the peak.” If your case is RA-constrained, your charge/discharge prices must reflect that constraint. Otherwise, your BESS Merchant Energy Arbitrage becomes an unrealistic upside story that won’t survive diligence.

Ignoring losses (or applying them inconsistently). Your charge energy should be larger than your discharge energy once efficiencies and conversion losses are applied. If your model shows the opposite—or if it’s unclear where losses are captured—your BESS Merchant Energy Arbitrage math will be hard to defend.

Debt vs equity credit is not the same. Even when merchant assumptions are reasonable, lenders often apply haircuts (for example, partial credit to merchant cash flows in debt sizing). That’s not “pessimism”—it’s credit discipline. Build your model so it’s easy to separate the equity view (full merchant upside) from the debt view (haircut merchant cash flows), and you’ll get a much cleaner investment committee narrative.

If you keep these guardrails in place, your merchant overlay will read like a financeable structure—not a trading strategy.

Wrap-Up and Next Steps (Deal Lab + RVA Certification)

You now have the full blueprint for modeling BESS Merchant Energy Arbitrage in a project finance-style Excel framework: price forecasts → cycles → energy per cycle (charge vs discharge) → profit per cycle → annual cash flows. When you layer that on top of a contracted RA base, the result is a structure that can be compared side-by-side across scenarios—without hand-waving.

If you want to follow along hands-on, the BESS Deal Lab (Project Pulse) walks through the full build inside Excel step-by-step, including the supporting reference materials and the dashboard outputs that make results decision-ready. And if you want broader mastery beyond this single revenue stack—covering storage, renewables, debt sizing logic, sensitivities, and investment-grade outputs—this content also ties into the wider RVA Certification Program, where you build repeatable project finance modeling skills across multiple real-world deal structures.

FAQs

What is BESS Merchant Energy Arbitrage (in plain English)?

BESS Merchant Energy Arbitrage is when a battery buys electricity from the grid when prices are low (charging) and sells electricity back when prices are high (discharging). The profit comes from the spread between charge and discharge prices, but it’s reduced by real-world limits—round-trip efficiency losses, availability/curtailment, and how many cycles the battery can realistically run each year. In a project finance model, the key is turning that spread story into auditable annual cash flows: charge cost, discharge revenue, and net arbitrage profit.

How do you model merchant arbitrage revenue in a yearly project finance model (without hourly dispatch)?

You model it with annual “containers” that still respect the physics and constraints. Use two yearly price series—average charge price and discharge price—typically sourced from a market consultant. Then calculate the energy per cycle on an AC basis: energy needed to charge (higher) and energy delivered on discharge (lower) after efficiencies and losses. Multiply the net profit per cycle by equivalent full cycles per year (EFCs) to get annual charging costs, annual discharge revenues, and annual arbitrage profit. This approach avoids fake precision while still producing lender-clean, traceable cash flows.

What’s the difference between “cycles per year” and “equivalent full cycles (EFC)”?

“Cycles per year” is often used casually, but EFCs are the more precise concept for modeling. An equivalent full cycle represents the throughput of one full charge and one full discharge across the battery’s usable energy window—even if, operationally, the battery does partial cycles throughout the year. For example, two half-cycles can add up to one EFC. In a project finance model, EFCs are the cleanest way to control total annual energy throughput and keep merchant arbitrage revenue realistic—especially when the battery is constrained by other obligations like resource adequacy.

Why is the energy you buy to charge higher than the energy you sell when discharging?

Because of losses. When you charge, energy passes through the transformer and the power conversion system into the battery (AC → DC). When you discharge, it passes back out (DC → AC). Each direction has efficiency losses, and there can also be transformer/medium-voltage losses. The combined effect is the round-trip efficiency, so the battery must buy more MWh from the grid than it can deliver back. A lender-clean arbitrage model explicitly calculates both paths (charge energy and discharge energy) so the spread profit reflects real physics rather than idealized assumptions.

How should I choose a realistic arbitrage cycles-per-year assumption?

Start with what constrains dispatch in your specific structure. A fully merchant battery might target frequent cycling if spreads support it, but in many financeable deals the battery is committed to a contracted product (like RA), which limits how often it can chase spreads. In those cases, cycles are best treated as a conservative “headroom monetization” assumption rather than a maximum-possible throughput. Practically, you can triangulate cycles using: (1) market consultant views on expected dispatch and revenue capture, (2) operational limits and degradation warranties, and (3) lender conservatism—because even if equity assumes higher cycling, debt sizing often gives partial credit or haircuts to merchant upside.

Do lenders typically give full credit to merchant arbitrage revenues in debt sizing?

Usually not. Even if the merchant arbitrage logic is modeled correctly, lenders often apply haircuts or only partially credit merchant cash flows when sizing debt because spreads, dispatch, and cycling are more volatile and forecast-sensitive than contracted capacity payments. A practical approach is to separate views inside the model: use an “equity case” with full merchant arbitrage and a “debt case” where merchant revenues (or net merchant cash flow) are reduced by a lender haircut. That way the model cleanly shows why leverage differs between contracted-heavy structures and merchant-exposed structures.

How does a Resource Adequacy (RA) contract change merchant arbitrage economics?

RA turns a battery from a “pure trader” into a reliability product first. The project is paid primarily for accredited capacity (often via ELCC/NQC logic), and the battery’s dispatch flexibility can be constrained by RA performance expectations. That’s why RA + arbitrage structures usually assume fewer equivalent full cycles for arbitrage—because the battery can’t always charge at the lowest price or discharge at the absolute peak. In a good model, RA provides the stable cash-flow base, and merchant arbitrage is an overlay that monetizes remaining headroom rather than driving the whole business case.

What do I get from the BESS Deal Lab?

The BESS Deal Lab (Project Pulse) is a hands-on case study where you build a bankable battery project finance model end-to-end in Excel. You’ll work with a complete deal context (Information Memorandum), a structured model workflow (start file → fully built outputs), and the supporting reference material (the BESS “Secret Sauce”) so every assumption and calculation is understandable and defensible. The focus is not just “getting a number,” but learning a repeatable framework: how to translate commercial terms into clean cash flows, how to model capacity vs merchant revenue stacks, and how to present results in an investor-grade dashboard for real decision-making.

How does the RVA Certification Program connect to this merchant arbitrage topic?

This arbitrage model is one piece of a broader project finance skill set. The RVA Certification Program takes you beyond a single revenue stack and trains you to build and evaluate full investment-grade models across renewables and storage—covering structured cash flows, scenario analysis, debt sizing logic, sensitivities, and decision-ready dashboards. If your goal is to become the person who can walk into an investment committee meeting and defend assumptions, structure, and returns across multiple deal types, the RVA Program is the complete pathway—while the Deal Lab is the deep-dive, real-case application for BESS.